Watch our latest video blog episode as Jay Lewis and Josh Tagg discuss the recent announcements from the Canadian government that could significantly impact homebuyers, particularly those entering the market for the first time. In this informative session, Jay and Josh unpack the new changes to mortgage amortizations and the RRSP Home Buyers’ Plan, providing insights into how these could enhance affordability and stimulate the housing market. Whether you’re planning to buy your first home or are just curious about the current state of real estate in Canada, this episode offers valuable perspectives and detailed analysis tailored for potential buyers and industry watchers alike.

Stay tuned after the video for a detailed blog post where we dive deeper into these topics, exploring the implications and opportunities these changes bring to the Canadian housing landscape.

Understanding 30-Year Amortizations

The reintroduction of 30-year amortizations for high-ratio insured mortgages marks a significant shift in Canada’s approach to housing finance. Previously reduced to 25 years, the extended amortization period aims to make homeownership more accessible by lowering monthly payments, thus allowing first-time homebuyers to qualify for larger mortgages. This change is particularly targeted at those purchasing new homes, ensuring that the benefits are directed towards stimulating new home construction and addressing the housing supply shortage. This section of the blog will discuss the specifics of the policy, its intended targets, and the potential long-term effects on the housing market.

Impact on First-Time Homebuyers

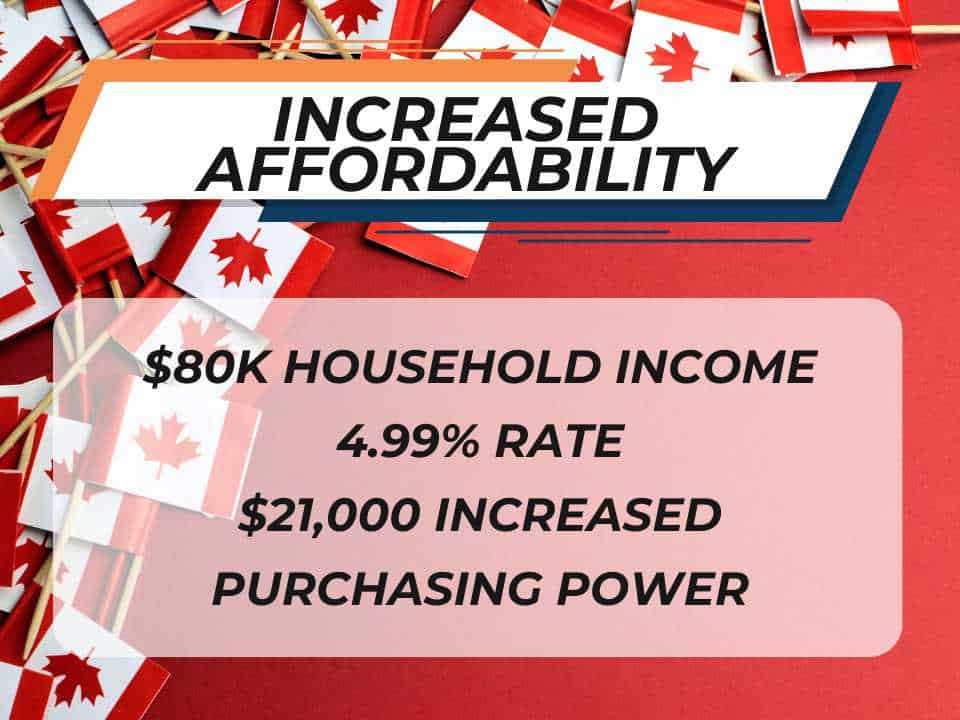

For first-time homebuyers, the updated policy could be a game-changer. By extending the amortization period, individuals can see a decrease in their monthly mortgage payments, making it financially easier to enter the housing market. Or, said differently, for the same monthly payment they can now borrow more money. For a family earning $80,000 annually, this translates into about $21,000 more purchasing power at current interest rates, and assuming a 5% down payment.

The Need for Increased Home Construction

Josh Tagg noted the necessity of increasing the supply of new homes to balance the market and stabilize prices. The targeted measure to extend amortization periods for new home purchases is intended to encourage developers and builders to ramp up construction efforts. This blog section will address the estimated increase in housing starts needed to achieve market equilibrium as suggested by the parliamentary budget office and discuss the challenges and opportunities this presents to the construction industry in Canada.

The Reality of Housing Affordability in Canada

Despite these positive changes, the question remains: Are these measures enough to combat the broader housing affordability crisis in Canada? This section of the blog will provide a critical analysis of the effectiveness of these policies in making homeownership a reality for more Canadians. It will consider regional disparities in housing markets, such as the differences between Edmonton and more heated markets like Toronto and Vancouver, and evaluate whether these policy changes could have a diversified impact across the country.

Challenges and Opportunities for Builders

The focus on new home construction presents both challenges and opportunities for real estate developers and builders in Edmonton and across Canada. With the government’s emphasis on stimulating the construction of new homes, developers are encouraged to increase their projects. However, as Jay Lewis pointed out, concerns about land availability and the readiness of serviced lots could pose significant hurdles. This section will discuss the potential risks and rewards for builders as they navigate the increasing demand for new homes and the logistical constraints of expanding urban development.

Analyzing the Impact on Edmonton’s Market

Although the housing crisis is more severe in other parts of Canada, Edmonton has its unique market dynamics. The local market has not experienced the same steep price increases seen in Canada’s largest cities, making it a relatively affordable option for many first-time homebuyers. This section will examine how the new government policies might specifically impact Edmonton, considering factors like local demand, pricing trends, and the availability of new housing developments.

Enhancements to the RRSP Home Buyers’ Plan

Another significant announcement is the enhancement of the RRSP Home Buyers’ Plan. The government has increased the withdrawal limit from $35,000 to $60,000 per person, enabling prospective homebuyers to access more of their saved funds for down payments without immediate tax penalties.

For those with higher RRSP savings, this will allow more Canadians to hit a 20% down payment, particularly in high-cost areas. In addition to the higher withdrawal limit, the government has also more than doubled the amount of time before the 15 year repayment of the RRSP must begin. Previously, repayment had to start in the third year, but now the wait can be a full five years with repayment beginning in year six. This will allow new home owners to get through their first mortgage term before they need to start repaying the RRSP loan which will be a nice break now with the higher interest rates on new mortgages in 2024.

Future Outlook and Government Monitoring

As Josh Tagg highlighted, while the changes are hopeful, they are unlikely to solve the housing affordability crisis completely. It’s a multifaceted issue that requires a multifaceted approach. This part of the blog will explore the potential future steps that could be taken by the government and other stakeholders to address ongoing challenges in the housing market. Additionally, it will discuss the importance of continuous monitoring and adjustment of policies to ensure they meet the intended goals of affordability and supply enhancement.

The recent announcements by the Canadian government represent a proactive step towards addressing some of the most pressing issues in the housing market today. While the reintroduction of 30-year amortizations and the enhancements to the RRSP Home Buyers’ Plan are promising, their success will depend on a range of factors, including the response from builders, the availability of land, and ongoing economic conditions.

These policy changes are designed not just to make housing more accessible, but also to stimulate economic activity through construction and increase the overall supply of homes, which could help to stabilize or even reduce house prices in the long run. As we continue to navigate these changes, it will be crucial for homebuyers, investors, and industry professionals to stay informed and adaptive.

For more regular updates about Edmonton Real Estate and Mortgages, be sure to subscribe to our blog channel at Edmonton Home Team. We look forward to keeping you informed and helping you navigate the ever-evolving real estate landscape in Edmonton and beyond.

0 Comments