Navigating the Waves of Canadian Mortgage Rates in 2024

In the ever-evolving landscape of Canadian finance, staying informed about mortgage rates can be the difference between securing your dream home and missing out. With the Bank of Canada’s latest announcement, Josh Tagg and the Mortgages for Less team at Axiom Mortgage Solutions have all the insights you need to navigate these changes. Their latest Mortgage Minute video sheds light on the current state of mortgage rates in Canada, offering valuable information for homeowners and potential buyers alike.

🏦 Bank of Canada’s Interest Rate Announcement

The Decision: Holding Steady

On April 10, 2024, the financial world turned its eyes to the Bank of Canada, awaiting its much-anticipated interest rate announcement. In a move that matched economists’ forecasts, the Bank decided to maintain the current interest rate at 5%. This decision keeps variable rate mortgages hovering around the 6.3% mark with most lenders, while fixed-rate mortgages stay close to the 5% territory, depending on the term and lender you choose.

Behind the Decision: Quantitative Tightening

The Bank’s choice to stand pat on interest rates comes amid its ongoing strategy of quantitative tightening. This approach marks a significant pivot from the pandemic era’s expansive monetary policies, where low-interest rates and bond-buying programs were the norms to inject liquidity into the market. Now, the focus is on allowing bonds to mature without renewal, reducing the Bank’s balance sheet and leaving market forces to dictate pricing. This shift plays a pivotal role in the rising mortgage rates we’ve observed over recent years.

📉 Economic Indicators and Their Impact

Inflation’s Downward Trend

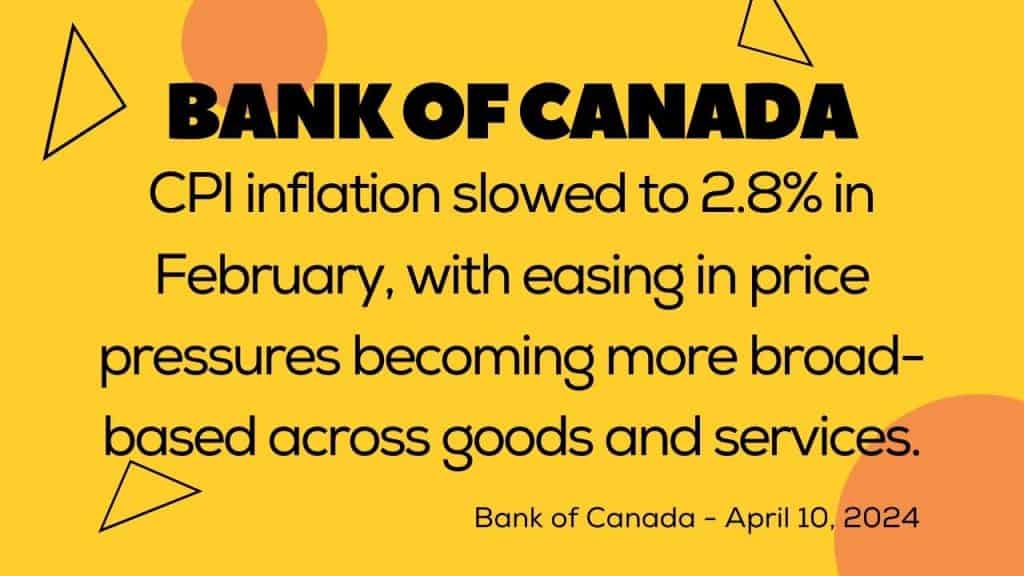

A silver lining in the Bank’s announcement was the mention of the Consumer Price Index (CPI) inflation dropping to 2.8% in February 2024. This decline is a welcome sign, signaling a broad-based easing of price pressures. While core inflation items (excluding volatile components like food and energy) have hovered above 3%, there’s a notable shift with some of these items beginning to edge lower.

The Future of Inflation

The Bank of Canada projects that inflation will reach its 2% target by early 2025. This forecast is crucial for mortgage holders and potential buyers, as it influences the Bank’s future decisions on interest rates. With the latest economic data suggesting a continued downward trend in inflation, there’s an optimistic outlook for those hoping for lower rates in the near future.

Stay tuned for the next section, where we’ll delve into the implications for fixed and variable rate mortgages, and what the U.S. economy’s performance means for Canadians. Remember, whether you’re renewing your mortgage, buying a new home, or just keeping an eye on the market, understanding these dynamics can help you make informed decisions.

Influence of the U.S. Economy

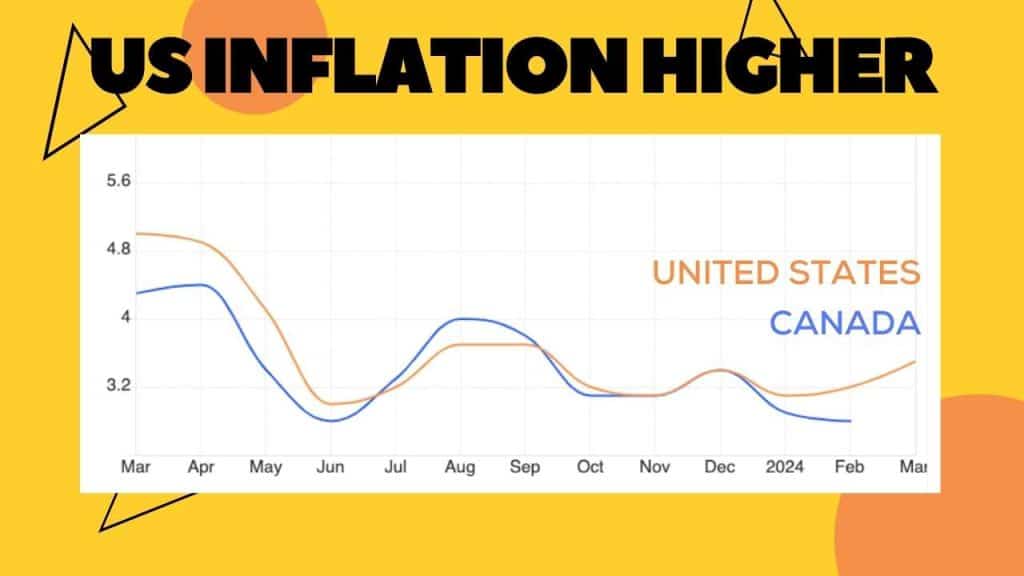

The economic performance of the United States has a significant ripple effect on Canada, particularly in terms of interest rates and inflation. Recent data showed U.S. inflation at a slightly higher rate than in Canada, with the U.S. Federal Reserve’s actions closely watched by Canadian policymakers. The interplay between the two economies means that while Canada might be poised to lower interest rates, it must tread carefully to avoid negative impacts on the Canadian dollar’s strength, especially important for provinces like Alberta, where oil exports are a key economic driver.

📊 Mortgage Rate Outlook: What’s Next?

As we navigate through 2024, the bond market’s recent movements suggest an 88% likelihood of an interest rate drop by the Bank of Canada come June 5th. This potential decrease could lead to a further dip in both fixed and variable mortgage rates, creating an advantageous scenario for those with mortgage renewals later in the year or considering entering the housing market. However, it’s also likely to exert upward pressure on home prices, as lower borrowing costs make buying more accessible.

Calgary and Edmonton, in particular, are already experiencing this upward pressure in housing prices. Prospective buyers and current homeowners should prepare for this possible scenario by consulting with mortgage professionals to navigate the changing landscape effectively.

In wrapping up today’s Mortgage Minute, we’ve covered the Bank of Canada’s latest interest rate announcement, the current economic indicators, and the potential implications for mortgage rates and the housing market. While the landscape may seem complex, understanding these factors can empower you to make decisions that align with your financial goals and home-buying aspirations.

We’re here to help you navigate these changes and opportunities. Whether you’re looking to buy, sell, or understand how these updates impact your mortgage, the Mortgages for Less team is your go-to resource for all things mortgage and real estate in Alberta.

🌟 Stay Informed and Empowered 🌟

For more insights and updates on the ever-evolving world of Albertan real estate and mortgages, make sure to subscribe to our blog channel @mortgagesforless. Our mission is to provide you with the latest information and tools to navigate the real estate market confidently. Whether you’re a first-time buyer, looking to refinance, or planning your next investment, we’re here to support your journey toward financial success and homeownership.

Thank you for tuning in to this edition of the Mortgage Minute. Until next time, keep dreaming big and planning smart for your future home!

Here Is a Transcript of Our Video:

Josh Tagg (01:12.95)

Well, hello and thank you for joining once again. Today is April 10th, 2024, and the Bank of Canada made an announcement regarding their interest rate. And as expected, the bank has decided to keep rates exactly the same for the time being.

Josh Tagg (01:46.414)

As expected, the Bank of Canada this morning had their announcement here on April 10, 2024, and they kept the rate exactly the same with a few clues and a few hints as to when the interest rate might start to drop.

Josh Tagg (02:03.318)

So this morning, the Bank of Canada’s rate announcement left the interest rate exactly the same at 5%. That leaves variable rate mortgages at about 6.3% with most lenders, and fixed mortgage rates are still sitting around the 5% mark, depending on which term and which lender you’re working with. The bank noted in today’s announcement that they are continuing with their policy of quantitative tightening.

That’s the opposite of what the bank did during the COVID pandemic, when it was essentially printing money and putting a lot of liquidity into the market by issuing bonds at very low interest rates. That allowed mortgage rates to get to all time, low records of around one and a half percent with many of our lenders. So the opposite’s now happening instead of selling off bonds. They are not renewing bonds that are coming up for maturity. So they’re.

getting rid of things on their balance sheet, which is making it so that the market has to do all of the pricing. And that’s a big part of the reason why fixed mortgage rates have come up over the last couple of years. However, with economic data that also impacts the fixed rate pricing. And we do see some impact from the inflation reports and the jobs reports and everything else that impacts both fixed and variable rate mortgage pricing.

So the bank of Canada did point out that CPI inflation in February did drop to 2.8%, which was amazing. And we’re super happy to see that. We have not yet received the March, 2024 data, but they did note that the easing of price pressures was becoming more broad based than it previously had been. So they do take a look at something called core CPI core inflation.

And some of the items in that have been running above 3% inflation, even as the overall inflation rate has been trending down. But some of those items that they were concerned about are now starting to nudge lower at around 3% in February, which previously been about a half of a percent higher. So that’s also good things. And when you look at the last three months revolving over the last few months, there is good indication that.

Josh Tagg (04:21.026)

those are going to continue to trend downward. The bank expects that the inflation will hit its target of 2% by early in 2025. So we are on track, and that’s a good thing. And so that does help support our previous estimates that we would see the Bank of Canada start to lower its rate as early as next announcement, which will be on the 5th of June. As far as fixed interest rate pricing is concerned, you can see here over the last six months,

there’s been some dips in the pricing, but then some upward pressure as well. We are seeing a five year fixed interest rates under 5% again, after they increased to almost 6% later last year. And so what we’re seeing now is with the US strong inflation, their numbers are coming in a little bit higher. Right now, we’re seeing the US 10 year fixed bond rates. That’s the green line on your screen.

those are starting to trend back up and Canada’s five-year bond rate very closely mirrors its movement. While the rates aren’t exactly the same when one goes up, one goes the other goes up and when one goes down the other tends to go down and Canada being so much smaller than the United States we’re not the ones causing the other to move so Canada’s rate is heavily impacted by what goes on in the United States. Their inflation rate this morning they released the data it came in high.

at three and a half percent. Meanwhile, Canada’s most recent reading was at 2.8 back in February. Now in February, the United States rate was also higher than ours. But with that upward pressure, what that means is that the United States, the US Fed may hold off a little bit longer before it starts to decrease its interest rate. And that has an impact here in Canada because if the Bank of Canada lowers its interest rate, it’s gonna have a negative impact on the strength of our dollar.

And while that’s great for Alberta when we’re exporting oil in us dollars, it’s not so great when we’re importing everything else, including our food, because that is sold and traded in us dollars. And so it makes everything a little bit more expensive and we’ll have some upward inflationary pressures. So the bank of Canada can start lowering its interest rate before the us fed does, but it can’t do too much if the us fed isn’t also doing something similar. So where does that leave us? Well,

Josh Tagg (06:40.718)

Nobody expected an interest rate drop today. There’s maybe a sliver of hope among a few, but not really. We’re still pretty strong on expecting it to be in June. Within the last few days, the bond market has been pricing in an 88% chance of a June 5th rate drop by the Bank of Canada. And even if it doesn’t happen, then we should definitely see it by July 24. So

You can expect those to start coming down. Hopefully we’ll start also seeing the fixed rates continue their downward trend and you know what that’s going to cause upward pressure on home prices. Cause as the mortgage rates come down, we generally see upward pressure on home prices. Calgary is seeing a lot of upward pressure already. Edmonton’s doing the same. And so as rates come down, be prepared for home prices to go up. If you have a mortgage renewal later in the year, that’s awesome.

because it’s going to start to trend downward and it won’t be as expensive as it was for people who are renewing last fall. So that’s what I’ve got for you today. Thank you for tuning in. Thank you for listening. Please click on like, um, to the video so other people can see it as well. Please subscribe to the page. Maybe hit that bell so that you get notified as I have more updates here in the future. Thanks so much everybody. My team and I are looking forward to helping you. Talk soon.

0 Comments