Join us today as Josh Tagg and Jay Lewis discuss Canadian mortgage renewals in 2024 and beyond. What impact will this have on interest rates and decisions by the Bank of Canada. At least a few respected economists are telling us that rates are about to go down and a lot of mortgages are up for renewal in the next couple years.

Jay Lewis: We’ve seen some really interesting data this week on inflation and the numbers and how they’re reporting. What can you tell us about that?

Josh Tagg: So what I can tell you is actually last week when the inflation data came in for the month of October, it actually came in lower than expected. And a big part of the reason is energy costs have come down. So we had like 3.8% inflation was the number for September. They expected around 3.4 and it came down all the way down to 3.2%. So again, really close to the Bank of Canada’s range of 1% to 3%. I have a chart here just showing kind of what’s been normal over the last 10 years and if you take a look at it, it’s kind of ignoring the inflation peak after COVID happened of course. A lot of that was kind of between 1% and 2% actually and the few times that inflation went above the 2% mark is actually it correlates with times that we saw interest rates increase. So with it coming down that’s that’s a positive thing as we’re considering what’s gonna be happening with interest rates.

Jay Lewis: So I guess maybe for the bear share of our clients, because we have a ton of them, right, that are gonna be renewing soon, I’m guessing, it looks like the market’s got a big sort of renewal coming up. Like, what does this mean for them?

Josh Tagg: You know, actually, I put together a blog post earlier today and in that blog post, I quoted a well-known or renowned economist named David Rosenberg, he had an an interview that he had with Bloomberg and they were talking actually about exactly that.

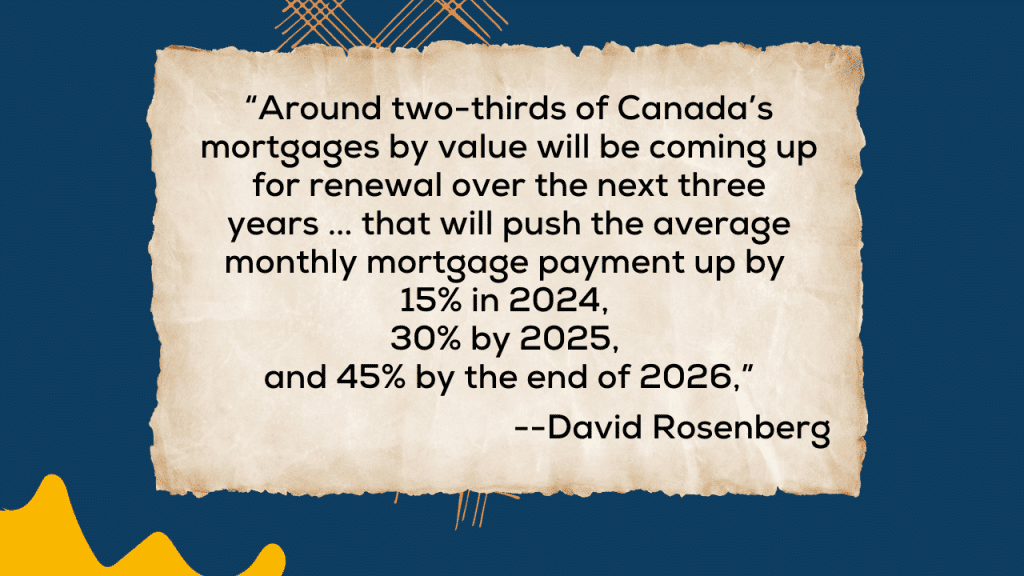

A lot of mortgage renewals are coming up in Canada and with people who kind of right now I guess we are looking at 2018 mortgages because most people take that five-year term. People in 2018 would have been locking in the mid 3% range and so with their renewing now around 5.5%, they are experiencing some definite increase in payments as a result.

In 2024, that would be 2019 mortgages renewing. We’re going to see about an increase in monthly payment of probably around 15% if rates remain similar to where they are today. But then if we get into 2025, which would then be 2020 renewals, rates were low in 2020. So we would be seeing more like a 30% increase in the payments for anybody who started their term back in 2020.

And the big one actually is in 2026. That’s when rates from 2021 are up for renewal. We saw five-year fixed rates between one and a half and two percent for quite a while. So those people will be seeing, assuming rates don’t change, a 45% increase to their mortgage payments which is just astronomical.

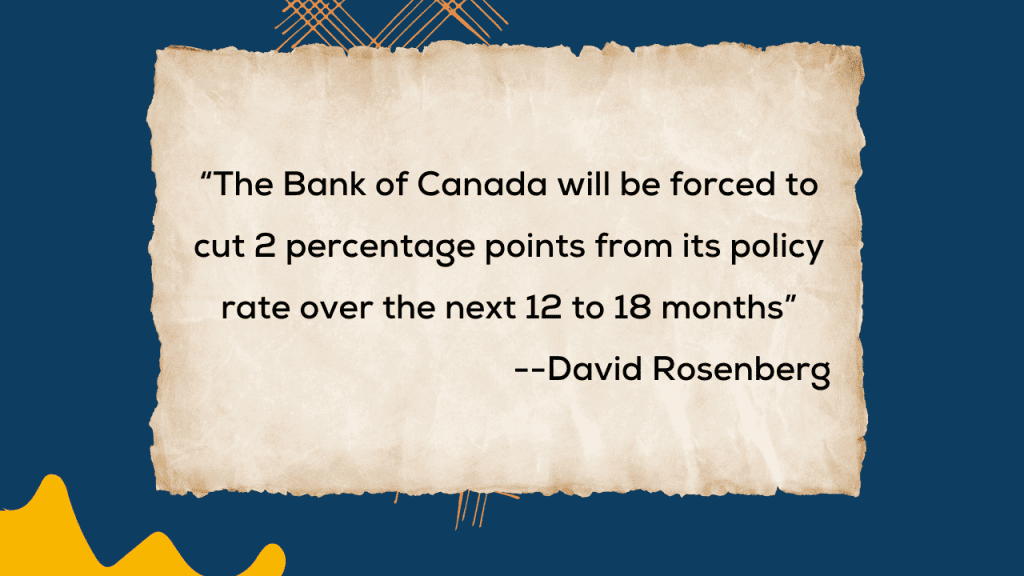

So he’s actually calling for the Bank of Canada to push toward lowering their rates by two percent over the next year or so. And in doing so we would see not only of course variable rate mortgages lowering, but along with that we would see the fixed rate mortgages also decreasing. The expectation is that there will not be any more increases and then April next year in the spring sometime is when most of the economists that were recently pulled by Reuters, they’re saying that around April is when we’re going to start seeing the first of the interest rate decreases happening. So we can cross our fingers that that’s the case and then kind of go with that.

Jay Lewis: Yeah, so that’s good news. If you’re a seller, right, like let’s get ready for the spring market, I think I’d be a little bit cautious if you’re just a buyer. So you, again, want to take caution about how long you wait to buy, not financial advice of course, but you kind of want to buy before everybody else does.

Josh Tagg: Yeah, and you know that’s maybe I think we kind of talked about maybe doing that video today but I think maybe next week would make sense that we can talk about what it would look like buying at today’s prices with today’s interest rates to drop say 1% but then how much more of an increase in home prices would that compare to?

Jay Lewis: Quickly, just one last question here and then we’ll get going back to work here. So, I’ve had this question from a lot of clients and they said like, you know, if I have a mortgage for five years and I go to renew, should the amount that I’m mortgaging lower and so will that offset a bit of what was happening when you get this interest shock or like what happens with the principal that their rates are based on?

Josh Tagg: For a standard renewal, what happens is, you know, let’s say five years ago you started with a 25-year amortization at 3.5% or something like that. Now we’re at a 20-year remaining amortization. So if we do see the payment or the interest rate increase, it will have an impact, but because it is a shorter amortization and there is a smaller balance owing, as you owe less and less money, the actual dollar impact of an increase in mortgage payments becomes less and less. So while it is not perfect, it is not a solution to everything, it does become less and less as you have fewer years remaining on your mortgage and as a bigger portion of your payment, it’s used toward being principal repayment instead of the interest on the loan itself.

0 Comments

Trackbacks/Pingbacks